Analysis and Studies - Studies

Global E-Banking Market: an insight

September 4th 2023

E-banking, also known as electronic banking or online banking, refers to the use of electronic channels, primarily the Internet, to conduct various banking activities and transactions. It provides customers with a convenient and accessible way to manage their finances, access banking services, and perform transactions without the need to visit a physical bank branch. The history of e-banking can be traced back several decades, marked by significant milestones in the evolution of banking services.

During the 1970s and 1980s, the concept of electronic banking started taking shape with the emergence of telebanking. Banks began utilizing computer systems and telephone networks to provide customers with basic banking services over the phone.

As personal computers and the Internet gained prominence in the 1980s and 1990s, online banking started to expand. The early 2000s witnessed a significant expansion of online banking services. Banks began offering features like online bill payment, fund transfers, and online applications for loans and credit cards. Improved security measures were implemented to safeguard customer information.

As personal computers and the Internet gained prominence in the 1980s and 1990s, online banking started to expand. The early 2000s witnessed a significant expansion of online banking services. Banks began offering features like online bill payment, fund transfers, and online applications for loans and credit cards. Improved security measures were implemented to safeguard customer information.

The rise of smartphones and mobile technology in the 2000s led to the development of mobile banking. Mobile applications allowed users to access banking services directly from their smartphones, providing greater convenience and accessibility.

Today, e-banking has become an integral part of the banking industry, revolutionizing the way customers access and manage their finances. Continued technological advancements and increasing digital adoption are expected to drive further innovation in e-banking in the future.

E-Banking Market: an insight

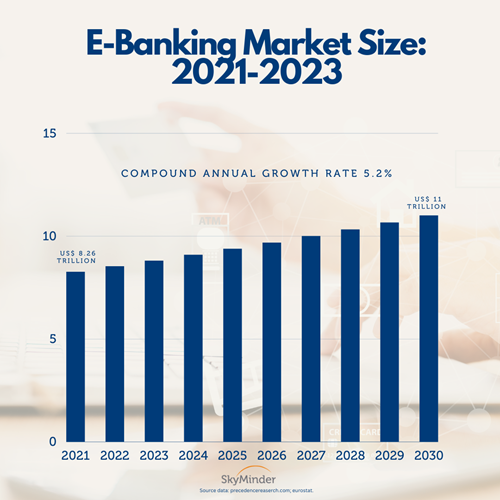

In 2021, the market size of e-banking was estimated at USD 8.26 trillion, and it is projected to reach approximately USD 11 trillion by 2030. The market is expected to experience a compound annual growth rate (CAGR) of 5.2% from 2022 to 2030.

In 2021, the market size of e-banking was estimated at USD 8.26 trillion, and it is projected to reach approximately USD 11 trillion by 2030. The market is expected to experience a compound annual growth rate (CAGR) of 5.2% from 2022 to 2030.

E-banking refers to the use of the Internet for electronic payment systems, enabling customers to access banking services online. It offers a convenient and secure way to perform various banking functions, eliminating the need for frequent visits to the bank. E-banking services, such as net banking portals, require secure login credentials for access. It is widely used by individuals, institutions, and businesses to conduct financial transactions, access account information, and explore different financial products. E-banking encompasses services like mobile banking, Internet banking, debit cards, ATM transactions, phone payments, and point-of-sale transfers.

The COVID-19 pandemic has significantly boosted the e-banking sector. With worldwide lockdowns in place, people increasingly relied on Internet services for their banking needs. Public awareness campaigns were conducted to promote the use of e-banking services during this time. Even though physical bank branches were open, social distancing measures and fear of the pandemic pushed people towards e-banking options. This has led to a surge in the market for e-banking in both developing and developed nations.

As people become more accustomed to online portals and other e-banking methods, the market for e-banking is expected to continue growing. Standardization of services and products offered by mobile applications has contributed to this growth. The widespread use of smartphones and increasing Internet accessibility have played a significant role as well. E-banking has effectively eliminated geographical barriers and provided a user-friendly online interface for banking services.

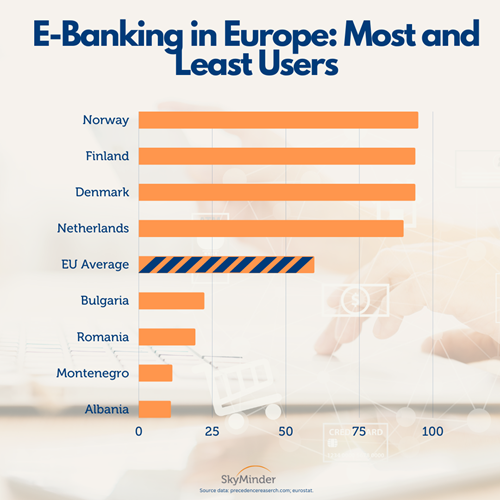

The European Continent is the fastest growing market for e-banking. However, there are many differences among the different countries. For instance, according to the data from 2022, Nordic countries, such as Norway (95.84), Finland (94.68), and Denmark (94.35) were the places with the highest share of individuals using the internet for internet banking (eurostat). On the other hand, countries in South and Eastern Europe were the ones with the lowest share. For instance, Albania (10.86), Montenegro (11.35), Bulgaria (22.44), and Romania (19.19) showed the lowest percentage of people using internet for online banking. Other major European countries, such as Germany (48.58), France (67.86), UK (80.41*), Italy (48.35), and Spain (69.60), showed different patterns.

The European Continent is the fastest growing market for e-banking. However, there are many differences among the different countries. For instance, according to the data from 2022, Nordic countries, such as Norway (95.84), Finland (94.68), and Denmark (94.35) were the places with the highest share of individuals using the internet for internet banking (eurostat). On the other hand, countries in South and Eastern Europe were the ones with the lowest share. For instance, Albania (10.86), Montenegro (11.35), Bulgaria (22.44), and Romania (19.19) showed the lowest percentage of people using internet for online banking. Other major European countries, such as Germany (48.58), France (67.86), UK (80.41*), Italy (48.35), and Spain (69.60), showed different patterns.

*data from 2020.